U.S. Economy

The U.S. economy entered 2026 on solid footing despite data volatility caused by trade effects and a government shutdown in Q4 2025. Underlying economic growth averaged 2.6% in the first three quarters of 2025, supported by resilient consumer spending and accelerated business investment in AI-related equipment and software. Job growth slowed significantly in 2025, though the unemployment rate remained low at 4.4% in December, as the labor market evolved into a low-hire, low-fire environment. Inflation measured 2.7% in December, above the Federal Reserve’s 2.0% target, with the Fed maintaining its policy rate at its January meeting after three consecutive cuts in 2025.

National Rent Growth

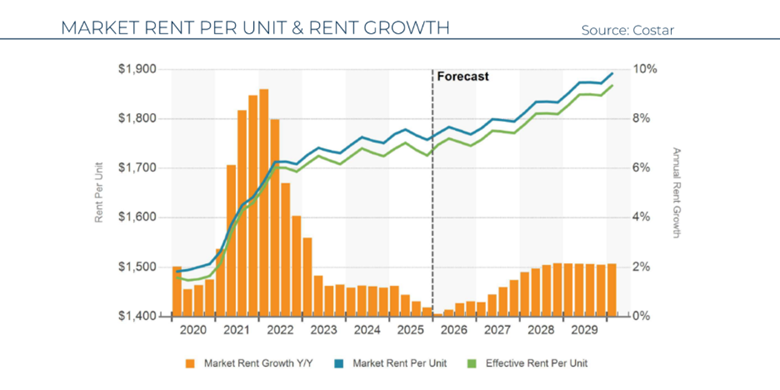

National apartment rent growth decelerated sharply in Q4 2025, with effective rents rising 0.5% year over year. The slowdown was driven by elevated supply and cooling employment, with rent growth varying significantly by building quality—1 & 2 Star properties led at 1.2%, while 4 & 5 Star properties, comprising 85% of recent completions, posted just 0.2% growth. Twenty-one of the top 50 markets experienced negative rent growth for 2025, with Austin down over 4% and Denver, San Antonio, and Phoenix declining 3% to 4%. Rent growth is expected to gradually accelerate in the second half of 2026, reaching approximately 1% by year-end, as moderating deliveries and steady demand create conditions for modest gains. The chart below illustrates the current rental environment along with forecasted growth and historical perspective (Costar).

Vacancy Rate

The national apartment vacancy rate for stabilized properties climbed to 7% in Q4 2025, increasing in the second half of 2025 after compressing slightly earlier in the year. Overall vacancy is forecast to plateau throughout 2026, though stabilized vacancy is expected to inch upward through Q2 2027 as the market absorbs the supply overhang from the past two years.

Apartment Demand

Apartment demand cooled in Q4 2025, with absorption totaling approximately 55,000 units, the first time below the 100,000 unit threshold since Q4 2022 and down from 144,000 units in the same period the prior year. This marks the end of a seven-quarter streak of absorption exceeding 100,000 units, bringing trailing twelve-month absorption to 400,690 units. The 4 & 5 Star segment dominated demand, representing 85% of Q3 absorption, with strength concentrated in New York and large Southern and Southwestern markets such as Dallas and Atlanta. Absorption is expected to stabilize at a more typical pace in upcoming quarters and is projected to overtake net deliveries in the second half of 2026, reversing vacancy trends and supporting firmer rent growth.

Apartment Construction

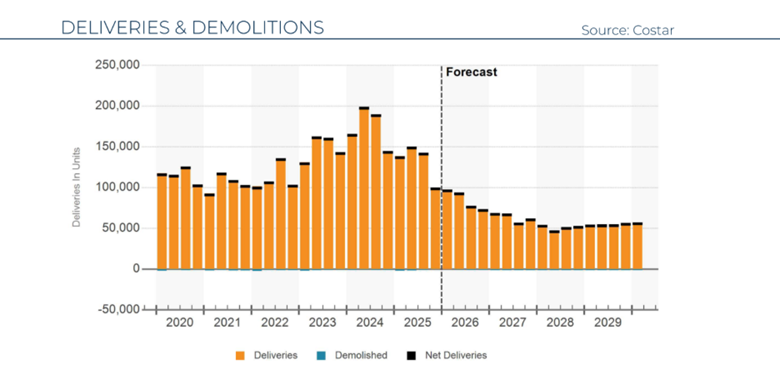

Apartment construction activity declined substantially in Q4 2025, with net deliveries falling below 100,000 units for the quarter, a decline of more than 30% from the same period a year earlier. Annual net deliveries totaled approximately 522,000 units in 2025, down 25% from the 2024 peak of nearly 696,000 units, with 2026 deliveries forecast to decline an additional 39% to approximately 319,000 units—the lowest level since 2014. The under-construction pipeline contracted sharply to 578,000 units in Q4 2025, nearly 50% below the cyclical peak of 1.18 million units in Q1 2023, driven by slower rent growth, higher capital costs, and tighter lending standards. This pullback is expected to help overbuilt Sun Belt markets absorb excess inventory and stabilize vacancy, with several markets including Phoenix, Atlanta, and Austin projected to see deliveries decline 33% to 50% in 2026.

The chart below highlights both the peak of quarterly supply along with the downward trend that began in 2025 and is now accelerating (Costar).

Apartment Sales

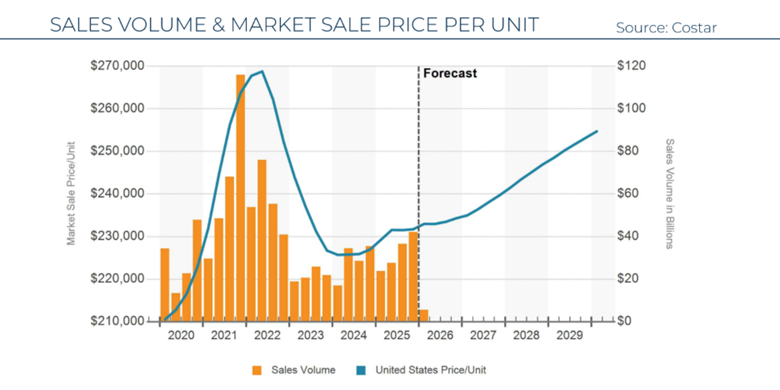

The multifamily investment market demonstrated clear signs of recovery in 2025, with transaction activity reaching approximately $135 billion—marking two consecutive years of growth and mirroring 2017 levels. Gateway metros led activity, with New York approaching $10 billion in trades and Los Angeles nearing $8 billion, while Atlanta and Seattle each recorded close to $6 billion. Private investors accounted for more than half of acquisitions in 2025, executing value-add and opportunistic strategies, while institutional managers represented roughly one-quarter of buyers, remaining selective and favoring cash-flowing assets in supply-constrained submarkets. Pricing has stabilized after declining 27% from the 2022 peak, with Costar’s value index now showing multifamily prices 21% below peak levels. Additionally, cap rates have also stabilized, clustering between 5.0% and 5.5% for 4 & 5 Star assets, 5.75% to 6.25% for 3 Star properties, and mid-6% to 7% for 2 Star buildings.

The chart below displays both quarterly sales volume and price per unit, which is a proxy for the markets view on values (Costar).

Apartment Financing

Apartment financing conditions improved markedly throughout 2025, supported by three Federal Reserve rate cuts and easing credit availability. Banks reported stronger demand for multifamily loans alongside modestly relaxed underwriting standards, creating a more favorable backdrop for capital deployment. Treasury yields have remained bound in the low-to-mid 4% range since late 2023, while high-yield spreads hover near cycle lows, signaling improved liquidity for borrowers. The Federal Reserve is expected to reduce rates by an additional 50 basis points in 2026 to reach its neutral rate, which should further support transaction activity and provide more accommodative financing conditions as elevated vacancy rates temper rent growth through mid-2026

Ackermann Markets and Target Markets

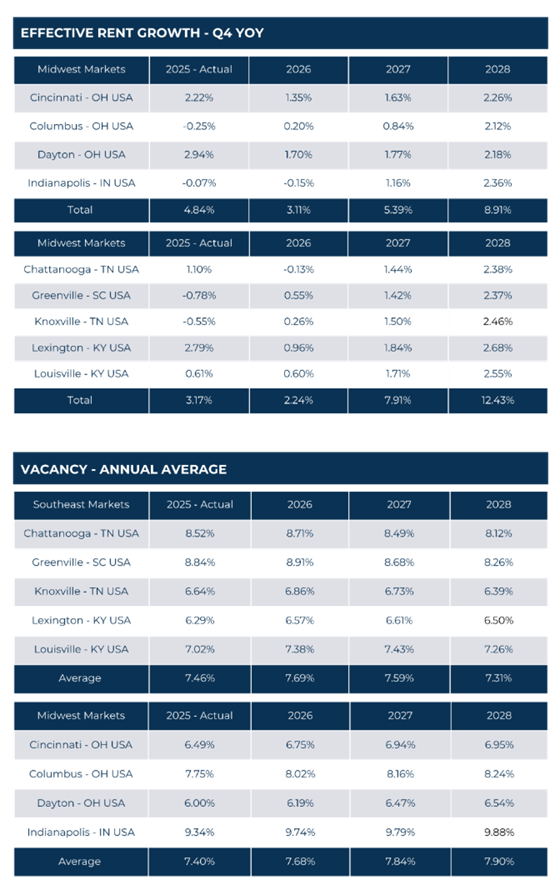

The Ackermann Markets and Target markets continue to generally outperform the rest of the country while also mirroring the region in which they are located. The Midwest markets have more positive rent growth in the near term and stable vacancy. In contrast, the Southeast target markets continue to contend with new supply which is driving rent growth down in 2026 while keeping vacancy stubbornly high. However, the Southeast markets are forecasted to catch up with their Midwest rivals in 2028 as job and population growth spur increased absorption without the accompanying apartment supply growth.

Columbus, Indianapolis and Lexington, KY are the exceptions to the rule. Columbus and Indianapolis have seen outsized construction that has kept rent growth low while Lexington has been an outlier in the Southeast for positive rent growth and low vacancy. The Costar data provided for each market below highlights regional trends.

Conclusions

The U.S. apartment market in Q4 2025 reflected a clear turning point as both supply and demand moderated from their cyclical peaks. The broader economy remained resilient with 2.6% underlying growth despite a government shutdown, though job growth slowed and inflation persisted at 2.7%, prompting the Federal Reserve to pause rate cuts after three reductions in 2025. Construction activity declined substantially with Q4 deliveries falling over 30% year-over-year and the under-construction pipeline contracting nearly 50% from its 2023 peak to 578,000 units, positioning 2026 deliveries to reach their lowest level since 2014. The investment sales market showed resilience with $135 billion in transaction volume for 2025, supported by improving financing conditions as banks relaxed lending standards and Treasury yields stabilized in the low-to-mid 4% range, while pricing remained 21% below 2022 peaks with cap rates clustering at 5.0%-5.5% for high-quality assets. Looking ahead, absorption is expected to overtake deliveries in the second half of 2026, stabilizing vacancy and supporting a gradual recovery in rent growth to approximately 1% by year-end.

INVESTING IN COMMUNITY TOGETHER for 88 years.